On January 31, 2025, Pepco filed its annual Bill Stabilization Adjustment (“BSA”) in the District. The BSA was first implemented in January 2010. The rationale behind the BSA was to remove the link between electricity use and utility revenue. Until now, the more electricity customers used, the more revenues Pepco received. Pepco argued that the previous rate structure created a disincentive for the utility to encourage customers to conserve energy since it lowered Pepco’s revenues.

Previously, the BSA was adjusted monthly and contained a 10% cap provision so that the monthly charge could not exceed 10 % of the expected revenue from each rate class. The BSA accrues the amount of expected revenue vs. what Pepco has collected and the under collection is then billed to rate payers. The BSA balances have been accruing at a significant rate, especially for the GT_LV class, which has a balance of $56 million in uncollected revenue.

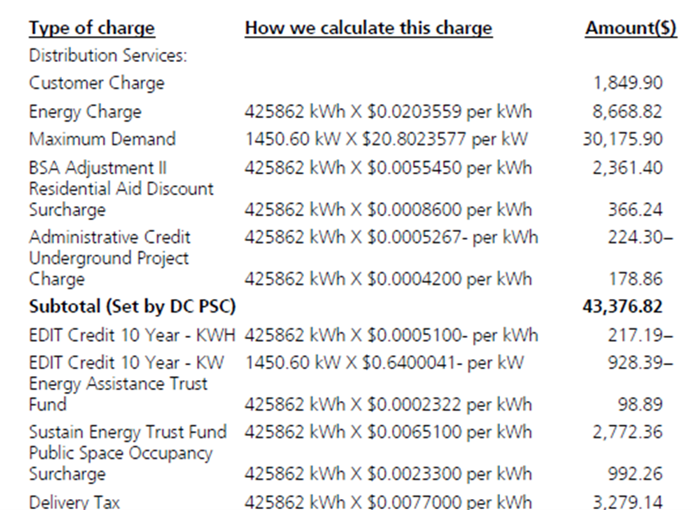

There have been several issues with the BSA that AOBA has testified about in the most recent Pepco rate case and other cases. Partly in response, the DC PSC authorized a change in the BSA in its most recent ruling:

- PSC directed Pepco to remove $15.3M balance, due to Pepco errors in the BSA demand billing determinant factor

- PSC also directed Pepco to create a regulatory asset to collect the BSA balances as of December 31, 2024 and collect those balances over the next 10 years.

The new BSA charge will be an annual charge as a separate line item on customers’ bills to be collected from March 2025 through February 2026. This charge will be listed as BSA Adjustment II on the bill. For a sample office building on the GT_LV rate schedule, the new BSA represents an increase of ~ $14K annually.

There will be a BSA Adjustment I that will calculate the over/under collected revenue for CY 2025. This will be another line item on bills beginning March 2026 through February 2027.